.jpg) |

| Alan Greenspan honored with Presidential Medal of Freedom |

Mathematical and statistically determined equations are not the economy. They are useful to some degree in formalizing a high level understanding of past behavior, but the models do not and cannot predict profound change, long-run policy impacts or important turning points. They never will.

Referring to the econometric models,

Wow! Not a psychologist, but how about being an economist? You are old school Mr. Chairman. You know how to do that."I've always considered myself more of a mathematician than a psychologist," says Mr. Greenspan. But after the Fed's model failed to predict the financial crisis, he realized that there is more to forecasting than numbers. "It all fell apart, in the sense that not a single major forecaster of note or institution caught it," he says. "The Federal Reserve has got the most elaborate econometric model, which incorporates all the newfangled models of how the world works—and it missed it completely."

Macroeconomic Model US Economy

During the financial crisis, I nailed it by putting two and two together, observing that household debt had risen to historically unprecedented levels at the same time home prices surged to previously unheard of highs in relation to incomes. Massive debt growth, much of it improvident, was unsustainably driving up home prices. Something had to break. When I saw that consumer savings rates effectively hit zero, implying that the credit bubble had no more room to grow, and I learned that that the first large wave of adjustable rate mortgages was resetting and high risk, subprime mortgages were beginning to default, I concluded that a historically immense de-leveraging process had begun -- in the spring of 2007. At the time I said we were going to have "the largest economic dislocation of our lifetimes." I knew from studying previous financial breakdowns and economic collapses that it would be profound. People laughed at me, mocked me or asserted that they weren't so pessimistic. They cited Ben Bernanke's (Greeenspan's successor and protege) repeated claims that the housing correction was "contained." They were incredibly wrong.

Now that Greenspan isn't working for the politicians and the bankers anymore, he is back to playing economist (a very good thing) and putting two and two together again, using insights and understanding on economic behaviors rather than being blindly dictated to by sum of the squared error calculations and goodness of fit measures.

In the book, he also ponders why the Fed failed to predict the financial crisis, where he himself went wrong and how that discovery has completely changed his worldview.

Mr. Greenspan's biggest revelation came one day about a year ago when he was playing with gross domestic savings numbers. What he found, to his surprise and initial skepticism, was that an increase in entitlements has closely corresponded to a decline in the country's savings. "We had this extraordinary increase in benefits, with each party trying to outbid the other," he says. "That practice has been eroding the country's flow of savings that's so critical in financing our capital investment." The decline in savings has been partly offset by borrowing from abroad, which brings us to our current foreign debt: "$5 trillion and counting," he says.

|

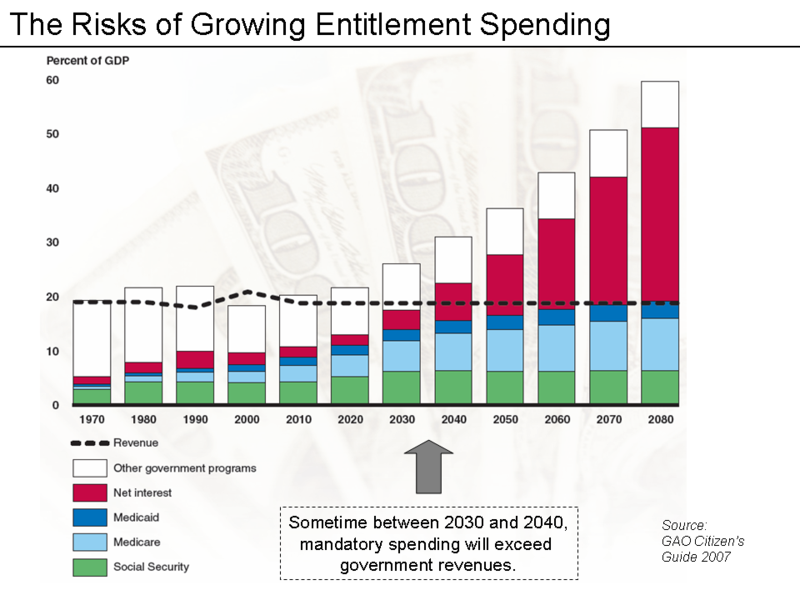

| Growth in Entitlement Spending. |

The bubble is being fed by the Fed printing a trillion dollars a year. Therein lies the next financial and economic crisis, and I daresay it will not be an econonometric model that tells us when it begins to implode, particularly since the first response will be to attempt to inflate the bubble all the more. Without a rapid and firm reversal, this is how the U.S. becomes Greece.

I am only referring to a stable market with respect to price. Not the way in which it is financed. Government support of home purchases in today's market is simply support of upper and middle class buyers to the detriment of those who cannot afford a house, and giving mortgage interest rate deductions to people of substantial means right out of the gutter.

ReplyDelete